First, I’d like to commend the SEC and its crypto task force for the tireless work they continue to undertake. It was an honor to participate in the Securities Status Roundtable, and I genuinely appreciate the turnaround in the SEC’s regulatory approach, particularly concerning openness, collaboration, and transparent public dialogue. I've never felt more optimistic about our ability to establish a thoughtful regulatory path forward.

As a takeaway from the roundtable, I want to note another pretty stark dynamic shift that has become apparent to me. As we switch from playing defense and begin to have a path forward on crypto policy, I find myself positioned as a moderate within these policy discussions for the first time. A rose—if I do say so myself—between the following two thorns:

Thanks for reading SHBrennan’s Substack! Subscribe for free to receive new posts and support my work.

- The Regulate-Everything-to-Death Camp. On the one hand, we have our traditional “kill it with fire” crowd – those who perceive securities transactions everywhere (to a hammer, everything is a nail), argue that Howey has no veritable limit in its ability to find securities transactions in any and all economic activities, and generally do not see value in creating compliant paths for crypto.

- The Libertarian Fever-Dream Camp.On the other hand, we have those who are (to different degrees) co-opting crypto as part of an attempt to liberalize capital formation. They are essentially attempting to skirt traditional capital markets by using crypto as a reg arb play. This side includes a couple of flavors of arguments – including, (1) the predicate contract crowd, (2) the secondary market transactions are not securities transactions crowd, and (3) the only yield bearing/value accruing tokens are securities crowd.

These two camps advocate policy positions pushed to opposite extremes. While they diametrically oppose each other in approach, they are equally unproductive in arriving at a balanced or effective approach to crypto regulation.

For instance, while approaching the issue of token taxonomy – the following things can be equally true:

The SEC’s stance—that an investment contract permanently infects the underlying asset—is simply untenable. The analysis of the asset must be separated from the transaction.

Equally problematic is the notion of crafting policy based on an artificially constrained view of Howey, including some sort of ‘four corners of the token’ rule.

Both of these positions falsely claim that they provide certainty and predictability to the market – the first only does so if you believe Howey has no limiting principles, including no outer limit in the ‘efforts of others’ prong and certainty and predictability means that there is no market (as we know it). I will also say it aloud – that for certain highly centralized projects that seek to stay centralized, it probably works fine in terms of certainty.

For example, purely hypothetically – if you wanted to disseminate tokens to retail where the blockchain was permissioned, supply was concentrated in the hands of a centralized business and the use case was facilitating transactions between banks, I think a securities designation for the whole scheme works fine from a policy perspective. The token serves no purpose in the hands of a class of can-never-be users and the whole model is in essence a ploy to issue a token as a junk synthetic-equity asset rather than have to avail yourself of traditional capital markets for fundraising like everyone else.

The second position attempts to force the ‘tokens are commodities’ analogy beyond its logical limit. While the analogy may have been useful in the context of collectibles and digital pet rocks without function (tokens of the varieties the SEC has already started sorting), it entirely falls flat in the context of network and DApp tokens. The latter taxonomies are tokens that have functions within a blockchain system – it becomes particularly important to the ‘regulatory certainty’ debate whether the issuer can change the inherent characteristics of the token in question, its function, mint additional multiples of supply or otherwise fundamentally change the tokenomics or the function of the system (and yes, it very much matters to this piece of the analysis whether the system is an enterprise system or is public and permissionless), etc.

To argue that the latter method could provide certainty to the market – rather than hand the market over for regulatory arbitrage plays – involves a willful suspension of disbelief. When I hear this theory advanced to conclude that logically the SEC has no jurisdiction over secondary market actors, it is easy to surmise (through a highly technical ‘who benefits’ analysis) that this theory has been concocted and advanced by trading platforms and other secondary market actors focused on ‘the token as product’ and shifting all regulatory burden away from themselves at the expense of investor protection and overall market health.

Taking a snapshot of a token as of a moment in time does not advance taxonomy (outside of the context of literal securities slapped on the blockchain). This amounts to a “pay no attention to the men behind the curtain” stance. Tokens within the network/ app token taxonomy are native to our digital paradigm. Their value is derived from their utility and thus the token doesnt meaningfully exist outside of the design of the system and the function/ interaction of the system with the token like an orange does. Pivotal to the analysis is whether these key aspects are either controlled by the issuer group or they are not.

Such a limited view intentionally ignores the risks of the system, network or web2 business to which the token is tied, treating them equally and thus incentivizing regulatory arbitrage, encouraging projects to issue valueless tokens as fundraising vehicles without genuine economic utility, consumer benefit or actually building the tech. This is just feeding retail to sharks.

So let’s just reduce these points and counterpoints to two big themes I noticed during the roundtable:

Continuing to Apply Howey Past Its Logical Limit.

Artificially Constraining Howey.

As we evaluate the best path forward among the options proposed at the roundtable with some arguing for more guidance around various Howey analysis factors (what is the outer limit of fundraising, what is the outer limit of vertical and horizontal commonality, others arguing for the SEC to take the stance that Howey should be viewed in a transaction by transaction manner), I would argue that the best path forward for the SEC is one that does no harm. Meaning, it provides a better outcome than the status quo – we need to be very cognizant of the fact that we are testing policy in production right now.

The ‘do no harm’ approach is exactly what we had in mind with the interim safe harbor concept but you can see the same restraint and balance of these competing interests in a number of the recent a16z proposals on airdrops and NFTs. These help unblock various economic activities that pose lower risks to investors and promote fair, orderly and efficient markets, which are all invaluable to advance as a next step.

But what they don’t do is argue for unilateral retreats of SEC jurisdiction in advance of a legislative framework. In fact, someone used to be fond of saying an industry cant long exist outside of the regulatory perimeter while maintaining an implicit policy stance designed to keep crypto outside this perimeter.

The continued arguments that Howey is going fine AND the newer ones that the SEC should not worry about secondary markets feel very similar to me to be honest.

If you are pushing positions that are ultimately asking the SEC to concede jurisdiction without there being a designated regulatory regime that covers it, you are essentially, absent legislation, asking for these activities to remain unregulated.

Next, when we look at the types of regulations that would be helpful in a secondary market, this stance becomes even more craven. They look very similar to what the SEC already administers: regulating underwriting/market makers, section 13d/g reporting, proxies, disclosures, the Williams act (ideally on steroids). In the secondary market, you need oversight/regs for the same reason you always do. We have countless examples of the market not regulating itself as secondary market actors engage regularly in market manipulation and otherwise destabilize the market.

Beyond the above discernible steps to provide interim relief, I will reference one of the comments from the roundtable, that “Howey was never supposed to regulate an entire industry” – yes, but this is really an argument to start engaging in rulemaking. To Chris Brummer’s point, it is a knock against the regulatory debt that has been accumulating more than it is against Howey.

However, a couple high level thoughts as we attempt to formulate rulemaking:

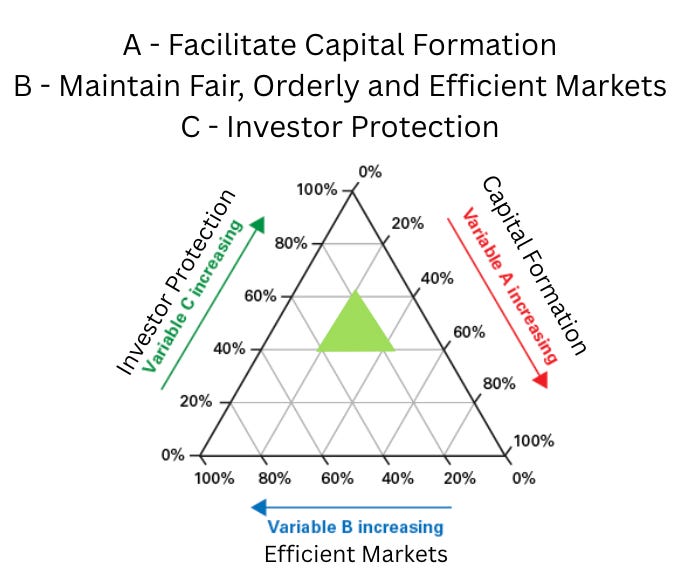

Policy is about Balance. Policy formulation is a process rooted in a social contract, where policymakers shape policy through a combination of rights and duties in pursuit of achieving societal goals. In the context of the SEC, it is bound by its three part mission. When pursued effectively, it is effectively about balancing three competing interests. Thus, the following is a good visual for evaluating the impact of competing proposals against these interests – generally, if a proposal aggressively pursues one of these elements in a zero sum manner and at the expense of the two others, it is not sound policy.

I understand it is tempting to rebel from a period where the SEC prioritized protecting investors… from any and all economic opportunities. But just as extremism over the past four years has been counterproductive and harmful, trying to swing the pendulum violently toward capital formation at the expense of the other competing interests will be equally damaging.

Both extremes are fraught with issues. The viable path forward requires acknowledging a broader scheme under Howey without pushing this view to an extreme that stifles genuine use cases and economic innovation.

Retaining the Principle - What is Broken in Traditional Capital Markets Must be Fixed in Traditional Capital Markets. For instance, the SEC liberalizing accredited investor rules, improving and expanding crowdfunding, liberalizing 701 and lifting overhead costs from traditional capital markets will flush out a lot of the opportunism in crypto policy discussions by those who see crypto as an escape valve for fundraising and trading activities with lighter touch regulations. As I discussed on the panel, tokens are a poor asset for investors versus equity and allowing crypto to be used primarily for regulatory arbitrage will harm all elements of the SEC mission and cause harm to crypto overall as you can only fundraise so much with junk assets and this industry is not sustainable if none of the technology gets built.

Remembering Why We Are Here. We started down this path to provide tokens that need network effects for the economic model to function a path to broad distribution and we have the time & space to design appropriate policy incentives — how about we actually leverage the opportunity instead of calling for regulatory accommodations for centralized models—or worse, demanding the same regulatory treatment as for decentralized ones. Such an approach would (continue to) skew incentives across the industry as well as traditional markets, diverting innovation and resources toward tokens as productized exit liquidity plays. It would undermine the core goal of building open, permissionless, and resilient infrastructure—the very foundation of what crypto is meant to achieve. It also isnt a viable path forward, much less likely to survive any political backlash we may face in …oh say, two years or so.

Securities laws have been a force function against decentralization. Even if you only look at the potential application of Howey from a defensive standpoint, you need to give teams a chance to reach ‘network maturity’ from a securities law perspective. I would argue that if you run a model where you are not capable of reaching exit where you are no longer the man behind the curtain determining all aspects of what the tokens are or could be tomorrow, you shouldnt be eligible for this model in the first place – the SEC may determine to find a path forward for these projects, but it should be cognizant of the fact they are at the very least, riddled with conflicts of interest and, at the worst significantly more likely to be a regulatory arbitrage play in their entirety.

A quick reminder that you dont have a god given right to bypass capital markets regs by issuing a valueless token and using retail investors as your exit liquidity. RIP Long Blockchain Corp. (f/k/a Long Island Iced Tea Corp.).

Taking a Break from Academic Echo Chamber Debates. Ever since The DAO Report was released, I've heard endless theoretical debates around the ‘correct’ interpretation of Howey, but ultimately, our personal views on correctness matter little, since courts have the final say. Academic debates are also more focused on ‘being right’ than driving good outcomes. In any event, as Lee Reiners noted, courts tend to apply Howey broadly, capturing larger schemes—and I don't think they're incorrect in doing so. Continuing to insist upon various narrowed interpretations of Howey isn't legally reliable or practically helpful, especially considering the threat that looms through aggressive enforcement by state securities regulators and plaintiffs' attorneys.

Decentralization Does Matter & Control Is the Right Lens. The level of decentralization of the model happens to be a pretty good barometer in analyzing whether the whole business and token model is a ‘scheme’. The decentralization analysis was always consistent with, and a gloss on, Howey and the safe harbor approach was necessary to bridge the issues securities laws pose to wide dissemination of tokens to users. Somewhere along the way people have started arguing “but what if they want to stay centralized” and generally replaced all thoughts of ‘why’ token with ‘wen token’.

Ultimately, tokens shouldn't solely serve as a loophole for traditional market frictions, nor should securities laws unecessarily impede genuine technological and economic use cases. On the one end of the spectrum, tokens replacing equity entirely as the sole value accrual mechanism in decentralized networks represent a fundamentally innovative organizational model and warrant clear, tailored regulatory paths distinct from traditional equity-based structures. On the other end of the spectrum, centralized businesses using tokens as a fundraising tool and additional value capture mechanism for insiders without genuine decentralization efforts are merely traditional businesses in disguise and shouldn't benefit from the same regulatory treatment.

While digital assets themselves don’t inherently confer traditional securities rights, the SEC must analyze the full context of their market introduction and ongoing issuer control. Dual-use tokens (in that they are intended to be used & we have trading markets for them) should remain within regulatory oversight until issuers no longer control the tokens' fundamental characteristics. It's critical to distinguish genuinely decentralized network tokens from tokens tied directly to centralized entities using regulatory arbitrage.

People have expressed frustration with the difficulty of administering a decentralization test but this is true of any principles based test. The safe harbor approach can fix this by offering a non-exclusive safe harbor (as takes place in other areas of securities law) involving a bright line test – and I think Miles Jennings is correct in his updated test focused on control.

All of the competing arguments on where to draw regulatory lines will ring hollow when you apply this lens. It is a two part analysis as well - whether the issuer group has designed the system to retain control and next a ‘de facto’ control test. Even if you design public and permissionless systems, they are prone to capture. When we look at the design test, again, you have to apply it broadly – I have recently heard a decentralization test being floated that only looks at whether the individual transactions are p2p and disintermediated.

This sounds like it was formulated by a centralized issuer trying to jump over the only hurdle they can. It falls victim to the issues raised by the control test and amounts to a test crafted by a centralized issuer as the only test they could possibly meet.

Either the tech is ‘cant be evil’ by design or you are in the same position you are always in with web2, a trustful model where you are depending on the team not to be evil. As I am sure this crowd will appreciate from all available evidence, people are pretty fucking terrible at refraining from being evil. This is after all, an impetus behind why this space exists in the first place.

Appendix - A Note for Professional Crypto Skeptics.

I would encourage those skeptical of our industry to change their stance from arguing for the application of securities laws to every type of activity just because you *could* and without regard to whether you *should* to having a focus on holding actors in this space accountable for failing to uphold the standards that the space purports to uphold. There is endless fodder for this exercise and it would be a net benefit to the space for you to use your platform for granular and constructive critiques.

Since this policy formulation exercise is happening with or without you, it would also be helpful if our assigned skeptics could abandon the stance that the application of Howey is ‘working perfectly fine’ as applied by courts. You are right that courts have had no trouble applying Howey extremely broadly and it would be helpful for you to point we're not in a position to do anything here than artificially constrain the SEC’s stance, which would come at a net harm.

There is more middle ground we can find as well - we can acknowledge in a taxonomy exercise that the token has to be separately analyzed but it may remain most helpful to look at the venture as a scheme when the token, its function and any future material changes made to the fundamental characteristics of either are controlled by, and thus entirely changeable, on the whim of the issuer group. The SEC can craft exemptive relief that is responsive to the risks once we pass these logical hurdles.

More broadly, I have seen critics say that permissionless and public tech infra is public by design but in practice will be captured — that decentralization will amount to nothing more than cartel behavior – none of them come up with policy solutions designed to prevent or disincentivize capture. Instead they continue to argue to kill it with fire. It hasn't been a particularly enlightened back and forth and at this point, serves even less of a productive purpose.

I have personally shaped (and reshaped) my views over time through interactions with thoughtful non-lawyers such as @fubuloubu, @ShadeUndertree, @tracheopteryx, @AFDudley0, and @0xMakesy. Additionally, I hold many in the legal community dear as accountability partners. Countless others, including @lefteris, @pcaversaccio, @dystopiabreaker, @functi0nZer0, frequently provide good-faith critiques of our space that have significantly influenced my perspective.

While I trust the internet will expand upon these lists, I strongly encourage engagement in good faith with dedicated actors like @l2beat, @SEAL_Org, @LlamaRisk, @ZachXBT, @Tayvano, and others who consistently strive to hold our ecosystem accountable. Their full-time commitment to holding our space accountable is invaluable, and we desperately need to listen to and leverage their insights.

More mainstream commentators like Molly White and Matt Levine (at times) also provide granular and substantive critiques. Embracing meaningful criticism and proactively seeking ways to improve the status quo as opposed to arguing ‘this is who we are now’ is essential. This is a crucial time for acknowledging the problems that exist and working actively to solve them.

Thanks for reading SHBrennan’s Substack! Subscribe for free to receive new posts and support my work.